%2024%20(1).png?width=150&height=161&name=Recognised%20CPD%20Badge%20(transparent)%2024%20(1).png)

In October 2023, MEPs approved legislation to protect consumers from misleading financial promotions. This law provides improved protection for those consumers who are not currently protected by sectoral regulations such as consumer credit and mortgages. The law focuses on distance contracts, for example, products or services bought online.

The EU requirements centre around:

- Pre-contractual information including the consumer’s right to cancel, charges for pre-withdrawal services, adequate explanations, and the right to human intervention

- Obligation to provide 23 key pieces of information such as instructions on how to cancel a service or product

- Informing the consumer if their call is being recorded

- Where a consumer cancels a service, firms can only request payment if the service was actually provided. Resulting in firms being obliged to return undue payments no later than 30 calendar days after the cancellation. Likewise, consumers too must return any money they may have received from a trader in the same period.

- failing to be transparent about their identities and motive when contacting consumers

- engaging in pressure selling and other poor sales practices, including offering gifts to unduly influence customers’ purchase decisions; and

- harassing consumers or being overly persistent in getting them to purchase financial products.

Depending on the regulated activities that a firm performs, and the products and services delivered, there are a myriad of local and international rules which continue to baffle some firms.

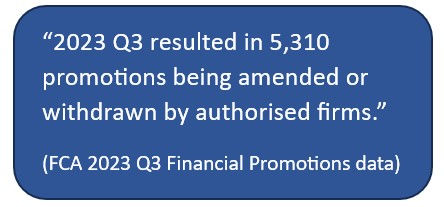

The FCA’s research has highlighted some fundamental issues, which resulted in the changes to the UK’s financial promotions regime.

- materials slipping through the net

- failure to understand who should review and approve their materials

- failing to realise that firms need to comply with regulations

- failing to gather evidence to demonstrate the materials were reviewed and approved, and completed by a competent person

- failing to appoint a competent person to review and approve financial promotion

If we consider some of the regulatory regimes that impact investment services or banking. These firms rarely work in isolation. They’re usually part of a distribution chain and may be selling products at home and abroad. They may use their own group entities to market their services or engage third parties. Regardless of the arrangements, firms need to track the rules that relate not just to the firm, but to the product or services being marketed.

- are identified as financial promotions,

- describe both the risk and rewards prominently, and

- contain clear, fair and not misleading information.

- maintain oversight of their representatives, whether that’s appointed representatives, agents, or distributors

- understand their marketing and sales processes,

- consider whether these third parties meet the standards required to demonstrate compliance with your obligations

Take a moment to consider the following steps; how do you currently demonstrate the following?

- Robust review process

- Ensuring accountability & competence of the Approver of financial promotions

- Demonstrating a comprehensive audit trail as well as appropriate sign off

- Improving due diligence on non-authorised firms, and

- Ongoing oversight of inhouse marketing and sales, and third parties

Firms need to reinforce their stance and be proactive where they discover failings. Failure to act reinforces the wrong behaviour and sets a standard that if unchecked could become the new norm. With the right level of oversight, you can improve your firm’s culture and standards to support and demonstrate compliance with the requirements.

Ruleguard is an industry-leading GRC software platform designed to help regulated firms manage the burden of evidencing and monitoring compliance. It has a range of tools to help firms fulfil their obligations across the UK, Europe and APAC regions.

The Ruleguard Financial Promotions solution allows firms to:

- manage and oversee their financial promotions in the context of the underlying regulations and relevant standards

- use configurable workflow tools to manage each stage of their promotions review process

- gather assurance data points that procedures are being followed as intended, and

- store and access supporting evidence to quickly answer queries for oversight and audit purposes.

If you’d like to learn more about the Ruleguard Financial Promotions Solution, please contact us for further information on:

Tel: 020 3965 2166 or hello@ruleguard.com

Ruleguard hosts regular events on a variety of regulatory topics. If you missed our webinar about Financial Promotions, you can still view it on demand.

Request a complimentary copy of our White Paper: A Guide to FCA Strategy: 2022-2025 click here.

Further resources:

See our blog page for further articles or contact us via hello@ruleguard.com.

Visit our website to find out more about how Ruleguard can help: https://www.ruleguard.com/platform