%2024%20(1).png?width=150&height=161&name=Recognised%20CPD%20Badge%20(transparent)%2024%20(1).png)

“ensure a higher and more consistent standard of consumer protection for users of financial services and help to stop harm before it happens”

The new Consumer Duty requirements are due to be finalised in July. It comes at a time when the FCA is keen to ensure that firms consider the impact of services and the suitability of products upon consumers.

This builds upon the existing requirements such as: acting in a client’s best interest, the treating customers fairly initiative and product governance requirements. Despite the current regimes additional obligations are required. The FCA has commented that it sees consumers struggling in the following areas:

- making informed or timely decisions due to lack of disclosure or transparency

- receiving unsatisfactory support from their provider

- buying products and services that are inappropriate for their needs, of inadequate quality, are too risky or otherwise harmful

The Consumer Duty aims to:

- tackle competitors who drive down standards

- provide greater assurance about how firms should treat consumers and flexibility on how they deliver good outcomes

- support future innovation by being clear about the standards required, whatever the product

This should be seen in the context of the regulator’s focus on encouraging good outcomes for consumers. Instead of a narrow focus on compliance with specific rules, firms are being asked to act in the spirit of the requirements. Firms need greater focus on delivering good outcomes and experiences for their clients.

Existing requirements

Firms are already required to treat customers fairly and abide by all of the Principles for Businesses, so what’s going wrong?

Some say that the abovementioned requirements are too broad resulting in firms have difficulty interpreting how they should comply. This is a challenge for firms, but it’s also a great opportunity to build an offering that fits a firm’s own business model and strategy. Firms should focus on ensuring that they have a strong governance framework. Under some regimes, such as MiFID II, firms need to treat remuneration and product governance in a specific way. Regulatory feedback indicates that firms may have set up committees to meet these requirements, but the implementation is not executed well. For example, challenge and debate should be evident from meeting notes and monitoring of activities should be supported with evidence. The rationale for how a decision has been reached may be missing.

It’s worth noting the FCA’s business plan highlights the need for firms to demonstrate specific outcomes which will be measured. In its feedback paper, A new Consumer Duty: Feedback to CP21/13, FCA stated that: How does this differ from the requirements under the TCF initiative where firms were asked to embed TCF and measure its effectiveness? As set out in the FCA's business plan, firms will be assessed according to their ability to deliver defined outcomes.

How does this differ from the requirements under the TCF initiative where firms were asked to embed TCF and measure its effectiveness? As set out in the FCA's business plan, firms will be assessed according to their ability to deliver defined outcomes.

New requirements

From July 2022, firms will have a set of new requirements relating to the Consumer Duty. These new obligations include:

A new Consumer Principle replacing Principles 6 and 7 for retail business: Firms must act to deliver good outcomes for retail customers.

Cross-cutting rules: how firms should act to deliver good outcomes and therefore provide greater clarity on regulatory expectations.

The cross-cutting rules require firms to:

- act in good faith

- avoid foreseeable harm, and

- enable and support retail customers to pursue their financial objectives

Rules relating to the 4 outcomes under the Consumer Duty: These key elements are instrumental to driving good outcomes for customers and relate to:

- the governance of products and services

- price and value

- consumer understanding and

- consumer support

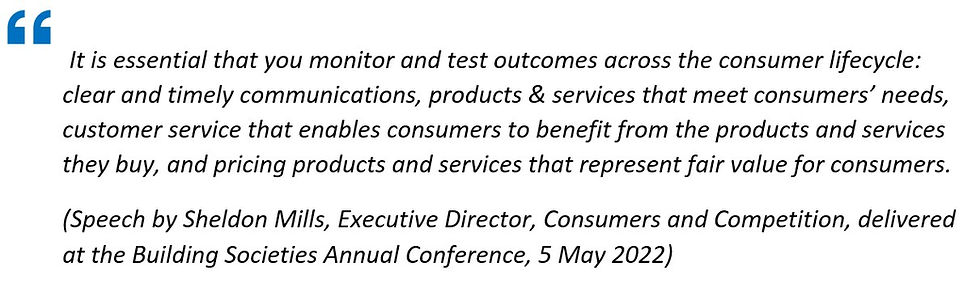

The FCA expects firms to monitor and test outcomes throughout the customer journey. Providing assurance to the board

Providing assurance to the board

Firms will need to develop an appropriate monitoring framework to provide assurance to boards and the regulator of compliance. Firms need to understand the likely outcomes for their customers from the products and services. These outcomes need to be assessed for the entire journey.

Firms need to monitor, assess, understand and be able to evidence the outcomes their customers are receiving. Where firms identify that consumers are not receiving good outcomes, they need to take appropriate action to rectify the causes.

How can Ruleguard help?

Ruleguard is an industry-leading software platform designed to help regulated firms manage the burden of evidencing and monitoring compliance. It has a range of tools to help firms fulfil their obligations across the UK, Europe and APAC regions.

Ruleguard has the potential to revolutionise what your firm understands by compliance monitoring and deliver best-in-class governance, oversight and management of compliance risk.

Evidence and approvals are gathered in real time, with responsible individuals signing off attestations within a framework designed for your firm. Documentation reviews and updates are managed automatically. Key compliance workflows can be designed directly within the solution, ensuring that MI outputs are available which directly provide stakeholders with an up-to-the minute overview of compliance results.

Please contact us for further information on: Tel: 020 3965 2166 or hello@ruleguard.com

Webinars:

Ruleguard hosts regular events on a variety of regulatory subjects.

To register your interest or learn more, please click here.

White Papers:

Request a complimentary copy of our White Paper on Best Practice in Third-Party Risk Management click here.

Further resources:

See our blog page for further articles or contact us via: hello@ruleguard.com

Visit our website to find out more about how Ruleguard can help: https://www.ruleguard.com/platform

Head of Client Regulation| Ruleguard