%2024%20(1).png?width=150&height=161&name=Recognised%20CPD%20Badge%20(transparent)%2024%20(1).png)

- New certification

- New duty of responsibility

- Seeking approval of additional senior manager functions

- Allocating new prescribed responsibilities

It required changes to governance, compliance and HR processes as well as preparation of additional documentation.

Fitness & Propriety and Misconduct Reporting:

With the previous Approved Persons Regime, regulators spent too much time examining a broad range of appointments. The SM&CR allows the regulators to focus attention on the key decision-makers.

- Improving Handovers – 94%

- Compliance & Ethics training – 85%

- Clarity on Board responsibilities – 79%

- Induction training - 72%

- Culture - 71%

- Succession planning - 61%

Accountability and Remuneration:

The PRA’s evidence indicates that during the period 2014-2018, approx. 400 material events prompted an adjustment downwards in the variable component of an individual’s remuneration. Like other regulated firms, insurers had an existing requirement regarding variable remuneration. However, the financial crisis of 2008 called into question the large bonuses paid despite large scale failures. Today, the supervisors emphasise the need to avoid rewarding senior managers for poor conduct. They also highlight the need for alignment between remuneration and risk management within the firms.

Individual vs Collective Responsibilities:

It’s important to note that the prescribed responsibilities under SM&CR are in addition to any duties held at the board level. The difference is that at board level, the strategic direction of the business is being addressed and then implemented on a day-to-day basis by the senior managers. In this way, SM&CR focuses on individual accountability for implementing strategic decisions. However, the board still has a role to play in collective responsibility that firms should not forget, something that the regulators are keen to emphasise.

Insurance firms should not lose sight of the obligations under the UK Corporate Governance Code or governance frameworks highlighted in the Insurance Core Principles.

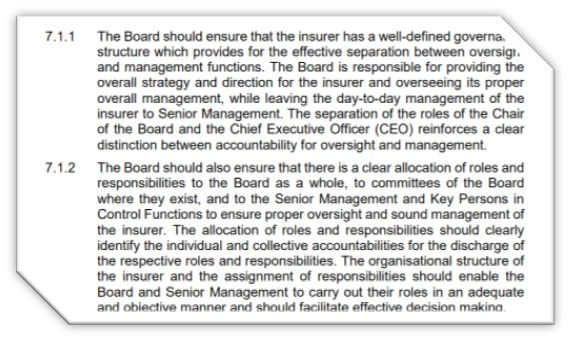

The Insurance Core Principles (ICP) adopted by the International Association of Insurance Supervisors (IAIS) note that governance frameworks should define the roles and responsibilities of persons accountable for the management and oversight of the insurer. This helps to clarify who possesses legal duties and powers to act on behalf of the insurer and in what circumstances.

Source: ICP 2019

For those firms that are part of a wider group, care needs to be taken in allocating senior management functions. For example, non-executive directors at the UK level may hold senior executive roles within the wider group. In this way, they may well be exercising direct influence over the regulated firm. In such cases, firms should consider assigning the Group Senior Manager (SMF7) to reflect the individual’s position better.

FCA’s Assessment:

The FCA undertook a review of SM&CR relating to banks and building societies. Like the PRA, it found that firms had embraced SM&CR. Overall there was greater clarity regarding accountability and more decisive direction from the top.

However, there is still room to improve. Firms should be looking at how they assess managers' competency and improve implementation below the senior manager level.

How Ruleguard can help you:

Ruleguard is an industry-leading software platform designed to help regulated firms manage the burden of evidencing and monitoring compliance. It has a range of tools to help firms fulfil their obligations across the UK, Europe and APAC regions.

Our end-to-end technology solution is designed to help firms reduce the cost and regulatory risk arising from compliance with Accountability Regimes. https://www.ruleguard.com/smcr

Please contact us for further information on:

Tel: 020 3965 2166 or hello@ruleguard.com

Ruleguard hosts monthly webinars, to register your interest or view past events please click here.

Further resources:

See our blog page for further articles or contact us via: hello@ruleguard.com

For more details, visit our frequently asked questions page.

Visit our website to find out more about how Ruleguard can help:

Contact the author

Head of Client Regulation| Ruleguard