.png?width=400&height=166&name=webinar%20-%20Client%20asset%20protection%20(1).png)

.jpg?width=400&height=166&name=shutterstock_2450801853%20(1).jpg)

.png?width=400&height=166&name=Compliance%20Monitoring%20White%20Paper%20(1).png)

%2024%20(1).png?width=150&height=161&name=Recognised%20CPD%20Badge%20(transparent)%2024%20(1).png)

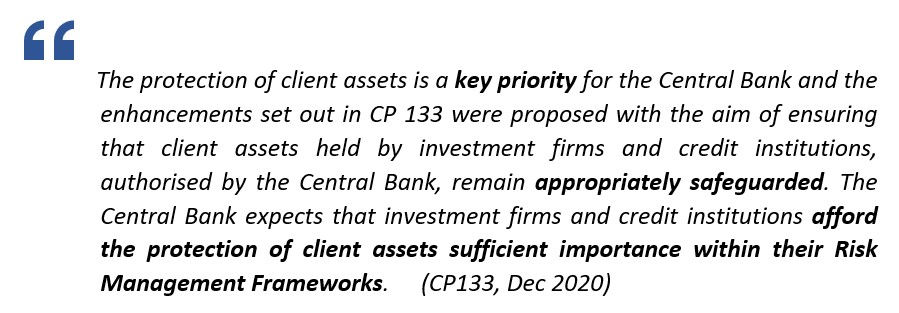

The Irish Client Asset Regulations (the CAR) were introduced to inspire public confidence and protect investors if an investment firm became insolvent. Revisions were made to the CAR in 2015 and today, we see Ireland preparing for further enhancements with the introduction of CAR 2022. These amendments should come as no surprise given that protecting client assets continues to be a regulatory priority worldwide, not just for the Central Bank of Ireland (CBI).

The current CAR introduced the following obligations:

- The CAR ‘Risk Management’ principle – all investment firms must develop and maintain a Client Asset Management Plan (CAMP) to document the risks to safeguarding client assets and how these risks are mitigated

- The CAMP must be challenged and approved by the Board

- Firms must appoint a Head of Client Asset Oversight (HCAO)

A couple of years after these measures were introduced, the Central Bank of Ireland (CBI) undertook a thematic review and issued its findings on how investment firms had implemented those requirements. This resulted in the CBI reminding firms, not only of the importance of this matter, but that accountability and responsibility for protecting client assets sits firmly with the governing bodies.

The CBI’s findings highlighted the crucial role that the Head of Client Asset Oversight (HCAO) plays within a firm. Specifically, that the HCAO must:

- work to develop the CAMP and embed it within the firms

- establish and maintain effective relationships with internal and external stakeholders

- ensure that protecting client assets is a top priority

Given the above duties, boards must ensure that they appoint a competent individual to perform this role. They must also ensure that the individual has adequate authority, resources and expertise to help them succeed.

Another area of regulatory focus was the CAMP. Here the regulators highlighted the importance of creating a comprehensive CAMP, embedded within the business, and which could be readily understood by independent reviewers. Additionally, firms must maintain the CAMP as a living document reflecting any changes to a firm’s business model. To support this aspect, firms must have a comprehensive risk identification process to capture and evaluate emerging risks.

Whilst the above findings were documented some time ago, it’s worth noting that investment firms must continue to pay due attention to these findings as these areas could be included in any future regulatory reviews. It's not just about CAR 2022, but also learning from earlier regulatory messages.

Preparing for CAR 2022

Some key enhancements to CAR 2022 include:

- extending the scope to include credit institutions undertaking MiFID investment business

- introducing client disclosure and consent requirements

- further clarity regarding segregation, and

- additional guidance regarding the content of the CAMP as well as the performance of reconciliations and treatment of discrepancies

For those firms who are already familiar with CAR, they’ll need to review and assess their processes and controls to identify any potential changes to ensure continuing compliance. Those firms that now find themselves within scope for CAR 2022, will need time and resources to identify and introduce appropriate systems and controls in a timely fashion.

How easily can you assess the impact of any business decisions and update your risk framework to reflect those changes? How do you provide assurance to your board of ongoing compliance with the client asset obligations?

Our Ruleguard solution

Ruleguard’s rules-mapping engine enables firms to map applicable business processes, risks, and controls directly to the client asset rules. The platform also allows firms to assign responsibility for the operation of controls to individuals and teams whilst also tracking completion of crucial activities. Control owners can be alerted via online attestations, checklists, and workflows to make sure that the controls are operating effectively.

Ruleguard is an industry-leading software platform designed to help regulated firms manage the burden of evidencing and monitoring compliance. It has a range of tools to help firms fulfil their obligations across the UK, Europe and APAC regions.

Please contact us for further information on: Tel: 020 3965 2166 or hello@ruleguard.com.

Webinars:

Ruleguard hosts regular events on a various regulatory topics.

To register your interest or learn more about our 2023 events, please click here.

White Papers:

Request a complimentary copy of our White Paper on Best Practice in Third-Party Risk Management click here.

Further resources:

See our blog page for further articles or contact us via hello@ruleguard.com.

Contact the author

Head of Client Regulation| Ruleguard